Estate Planning

Estate planning tips for unmarried couples

Estate Planning Tips for Unmarried Couples in New York At Morgan Legal Group, located in New York City, we specialize in estate planning, probate, elder

Estate Planning Tips for Unmarried Couples in New York At Morgan Legal Group, located in New York City, we specialize in estate planning, probate, elder

Estate Planning Advice for Same-Sex Couples in New York At Morgan Legal Group, located in New York City, we specialize in estate planning, probate, elder

Transfer Real Estate into a Trust in New York: A Comprehensive Guide At Morgan Legal Group, located in New York City, we specialize in estate

4 Key Mistakes Executors Often Make During The Probate Process At Morgan Legal Group, located in New York City, we specialize in estate planning, probate,

Probate Lawyer in Nassau, New York: Ensuring Smooth Estate Administration At Morgan Legal Group, located in New York City, we specialize in estate planning, probate,

Legal Experts Stress the Importance of Creating a Will At Morgan Legal Group, located in New York City, we specialize in estate planning, probate, elder

Probate Attorney in Nassau, New York: Ensuring Smooth Estate Administration At Morgan Legal Group, located in New York City, we specialize in estate planning, probate,

Creating a Legal Will in New York: A Comprehensive Guide At Morgan Legal Group, located in New York City, we specialize in estate planning, probate,

Understanding Asset Protection: Who Needs It? At Morgan Legal Group, located in New York City, we specialize in estate planning, probate, elder law, wills, and

Guardianship Attorney NYC: Protecting the Vulnerable with Expertise and Compassion At Morgan Legal Group, located in New York City, we specialize in estate planning, probate,

Guardianship Attorney in New York: Ensuring the Well-being of Your Loved Ones At Morgan Legal Group, located in New York City, we specialize in estate

Guardianship Attorney in Brooklyn: Protecting Your Loved Ones At Morgan Legal Group, located in New York City, we specialize in estate planning, probate, elder law,

Estate Planning New York Lawyers: Ensuring Your Legacy is Protected At Morgan Legal Group, located in New York City, we specialize in estate planning, probate,

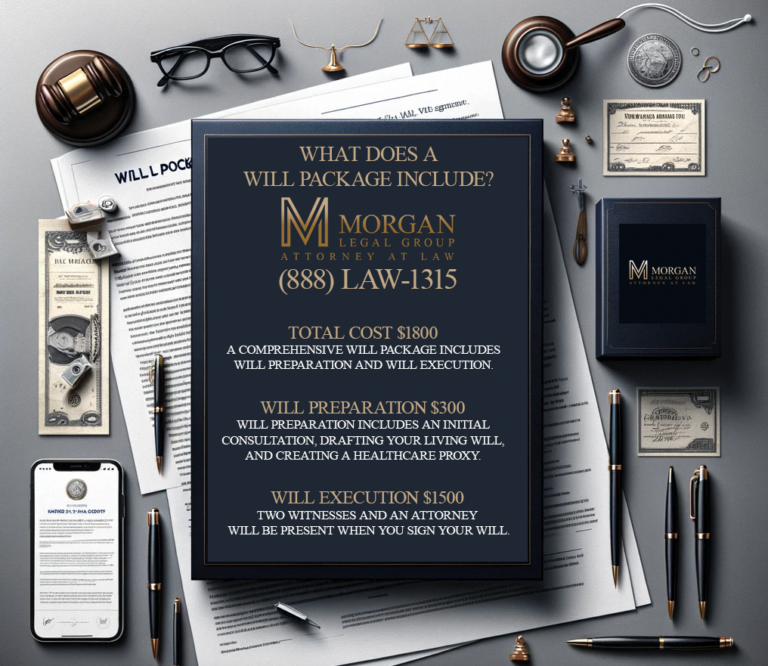

What Does a Will Package Include? At Morgan Legal Group, located in New York City, we specialize in estate planning, probate, elder law, wills, and

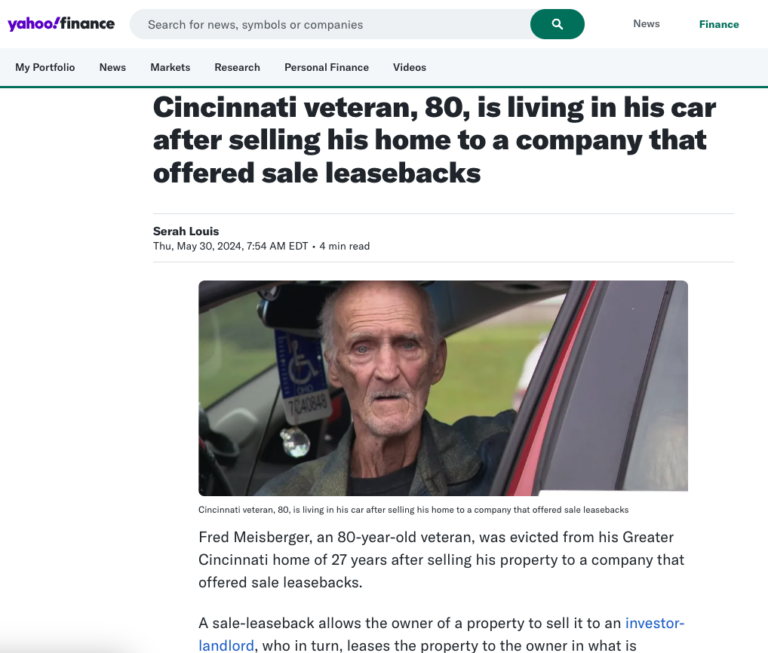

Cincinnati Veteran, 80, Living in Car After Sale-Leaseback Eviction Fred Meisberger, an 80-year-old veteran, has found himself living in his car after being evicted from

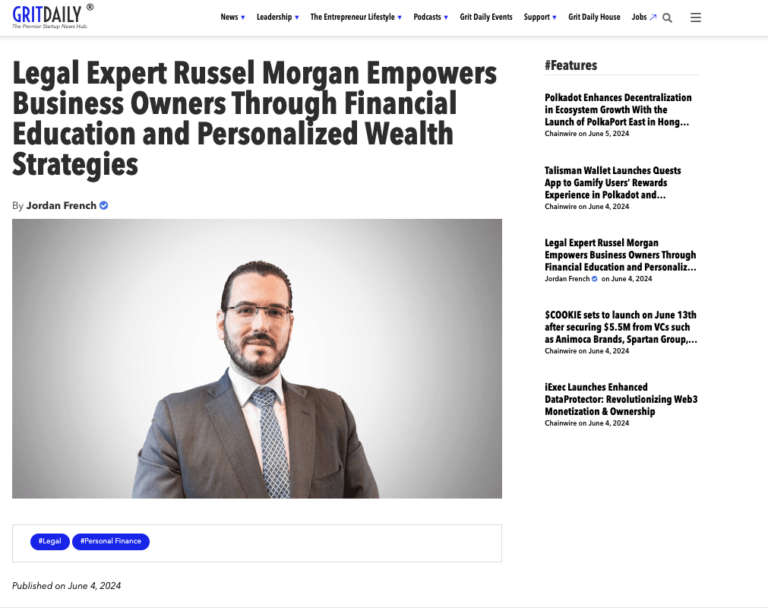

Legal Expert Russel Morgan Empowers Business Owners Through Financial Education and Personalized Wealth Strategies Russel Morgan, the CEO and founder of Morgan Legal Group in

Estate Planning New York Lawyer: Comprehensive Guide to Protecting Your Future Estate planning is a vital process ensuring your assets are managed and distributed according

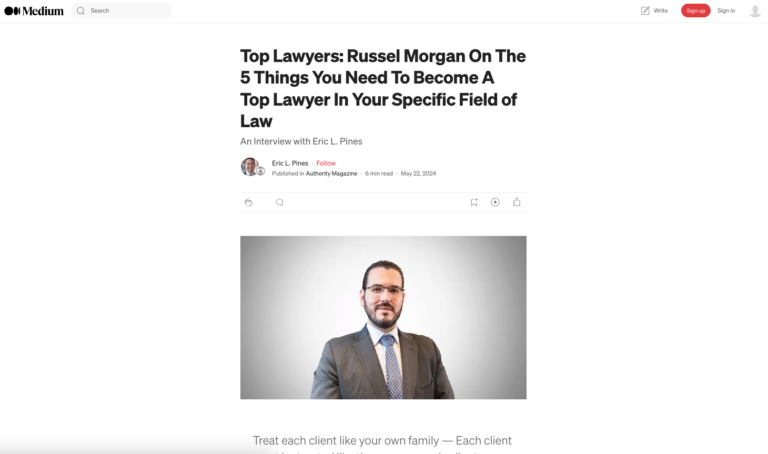

Russel Morgan: 5 Keys to Becoming a Top Lawyer Becoming a top lawyer in a specific field of law requires dedication, expertise, and a commitment

Estate Planning Attorney in Brooklyn: Comprehensive Guide to Securing Your Future Estate planning is a crucial process ensuring your assets are managed and distributed according

Guardianship Attorney in Long Island, New York: Protecting Your Loved Ones Guardianship is a legal process that appoints an individual to make decisions for another

Estate Planning New York Attorneys: Comprehensive Guide to Protecting Your Future Estate planning is a critical process that ensures your assets are managed and distributed

Probate Attorney Near Me 10007, NY: Expert Legal Services for Smooth Estate Administration At Morgan Legal Group, located in New York City, we specialize in

Wills Attorney in New York Brooklyn: Comprehensive Estate Planning Creating a will is one of the most important steps you can take to ensure that

Trusts Attorney in the Bronx: Your Guide to Comprehensive Estate Planning Planning for the future is crucial to ensure your assets are protected, and your

Understanding Guardianship and How Guardianship Law Attorney Can Help You Guardianship is a legal process designed to protect individuals who are unable to care for

Planning Your Estate 101 Estate planning is a crucial step in ensuring that your assets are managed and distributed according to your wishes after your

Life Insurance is Important When Planning for the Future When it comes to estate planning, life insurance plays a crucial role in ensuring that your

Estate Planning Lawyer: Comprehensive Guide to Estate Planning in New York Estate planning is a crucial process that ensures your assets are managed and distributed

Building Your Estate is Hard Work. Protect it with Asset Protection Planning Creating and growing your estate takes dedication, strategic planning, and hard work. However,

3 Times You Need a Probate Lawyer On Your Side The probate process can be complex and emotionally taxing, especially when you are dealing with