Before you undertake a task, let say book a flight you’ll conduct a little research, right? The same goes for an estate plan. Before you go ahead with your estate plan, it is wise that you understand what an estate plan is and the processes involved.

Estate Planning Explained

Estate planning is definitely not as exciting as planning for a vacation in Bahamas or a picnic on one of those serene and beautiful landscapes. However, even if it is not cable of providing you with the instant gratification you s much desire, this lone plan can help secure your future and the future of those you care about.

Estate planning in a nutshell, is all about making preparations for the transfer of your assets after your death. It consist of plans designed to ensure that you have a say on who inherits your assets. This plan can also be beneficial in the event that you become incapacitated, seriously ill, or unable to communicate.

Estate Planning Process

The estate planning process consists of three steps and they are:

First Step: The first step in the estate planning process is to identify your assets. These assets includes the assets you own and those in a superannuation fund, jointly owned assets, assets owned by trusts or companies, etc.

Second Step: The second step in the estate planning process is the identification of likely risks you wish to prevent, such as incapacitation, the possibility of a beneficiary becoming bankrupt or getting a divorce, etc.

Third Step: The last step in this process involves the creation and the implementation of plans and strictures that contains your entire assets and considers flexibility to include potential alterations, risk reduction, tax reduction, including success problems.

It is very safe to say that this last process is the most challenging of all. To ensure you have no problem when executing the last step, ensure you contact your financial planning, accounting, and legal advisers.

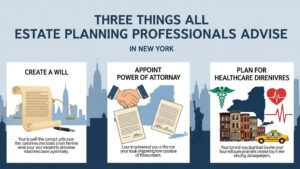

Though a will is a very common estate planning element, there are still other important documents that are as important as a will. A will covers just estate assets owned in your name like your properties, shares, bank accounts, etc. A will doesn’t cover non-estate assets like superannuation (if a beneficiary is not selected to the estate) assets in an inter vivos trust or insurance policies.

It is never too early to create an estate plan

When it comes to estate planning, there is no such thing as “too early.” Provided you are eligible to make an estate plan, and you have a few assets you would love to transfer to certain individuals after your death, it is best you contact an estate planning attorney make a plan.

You can always update your estate plan if you acquired a new house, a car, business, or got divorced. An estate planning attorney can help you update your estate plan, so, there is no excuse as to why you shouldn’t make that plan early.

Why is Estate Planning so Important?

Many people are yet to see the importance of estate planning. In fact, in the U.S lots of people die each year without drafting an estate plan, or even creating a will. The consequences of this terrible act, will be experienced by the family and loved ones of these estate owners.

Creating an estate plan is very important. In fact, I cannot emphasize how important this plan is to not just you, but to your family and loved ones.

Failure to create an estate plan when alive will likely haunt you when you become incapacitated. It will also affect your family when you eventually kick the bucket. There will be lots of court hearings to decide how your properties will be shared. Your estate will surely undergo probate which can be difficult, expensive and time-consuming, In a nutshell, failure to create an estate plan is a very terrible mistake

Contact us

If you need an estate planning attorney for your estate plan. Or you need advice on how to cut down estate taxes, don’t hesitate to contact our office.